Is China’s Digital Yuan Already Obsolete? The Rise of Yuan-Backed Stablecoins Explained

Share

Key Takeaways

e-CNY has scaled rapidly but struggles to compete with Alipay and WeChat Pay for daily retail use.

Beijing is developing yuan-backed stablecoins to expand RMB use in cross-border trade.

Hong Kong’s Stablecoin Ordinance provides a regulatory framework for safe issuance and redemption.

A dual-track approach positions e-CNY for domestic control and stablecoins for international growth.

China’s e-CNY, the country’s central bank digital currency, has grown rapidly at home through pilot programs and retail adoption, but it still struggles to gain traction beyond mainland borders due to capital controls and limited convertibility. At the same time, a new path is opening.

Beijing is weighing yuan-backed stablecoins to push the renminbi (RMB, China’s currency) into global payments and trade. The result looks less like a replacement and more like a double-back strategy.

The e-CNY remains the domestic rail. Beijing is signaling that it supports using regulated yuan-pegged stablecoins, and Hong Kong has already passed clear rules to allow them.

Together, this shows China is serious about using stablecoins for cross-border trade and offshore payments.

This article explains why the e-CNY, China’s central bank digital currency, may not be enough on its own to globalize the yuan and how yuan-backed stablecoins could complement it.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

China’s central bank digital currency (CBDC) has reached scale at home: over 180 million wallets have been opened and cumulative transactions hit ¥7.3 trillion ($1.02 trillion) by mid-2024.

The Bank for International Settlements (BIS) Innovation Hub reports that the e-CNY is already technically ready for cross-border settlement through projects like Multiple Central Bank Digital Currency Bridge (mBridge), which reached the minimum viable product (MVP) stage in mid-2024.

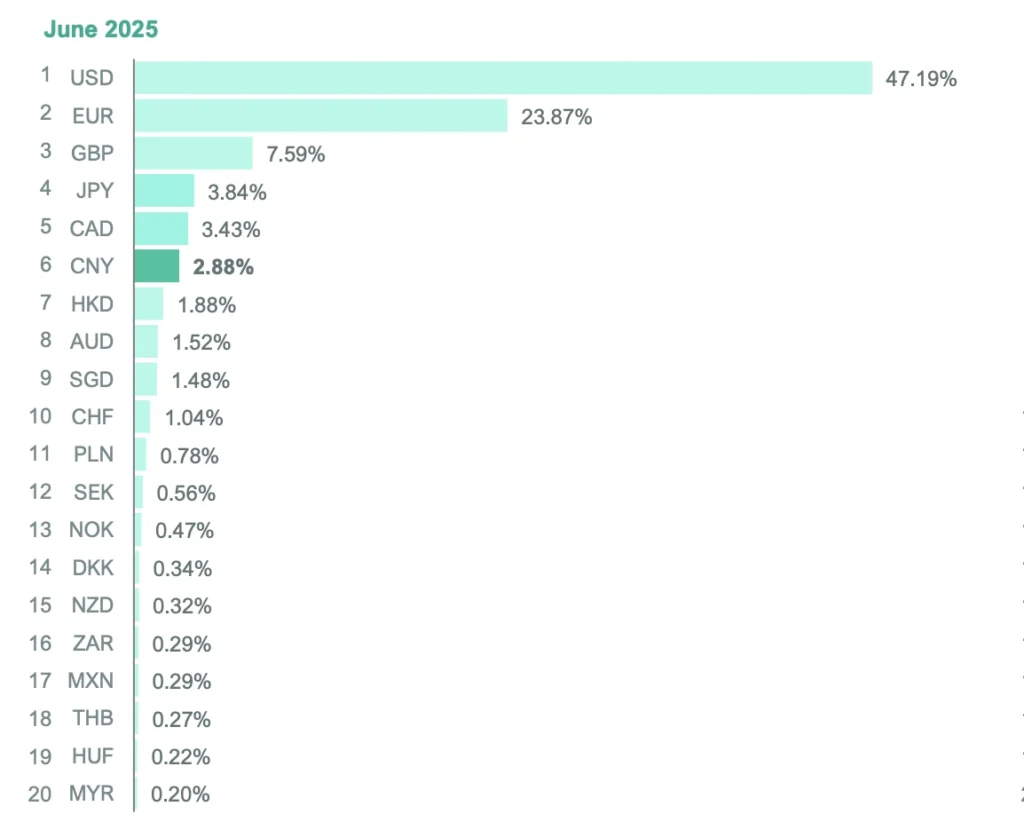

RMB’s share as a global payment currency | Source: Swift

Yet the RMB’s share of international payments was only 2.88–2.89% in mid-2025, ranking sixth globally behind the US dollar (USD), euro (EUR), British pound (GBP), Japanese yen (JPY), and Canadian dollar (CAD). This shows that while e-CNY works at home, it has not broken into global usage at scale.

Domestic Adoption: E-CNY Gains Scale but Struggles With Daily Use

China’s e-CNY is expanding across cities and services. It runs on a state-managed infrastructure with offline payment support, tiered digital wallets, and no need for a commercial bank account for small balances. However, adoption remains uneven in everyday life.

The currency is used in 1.3+ million scenarios, including utilities, transportation, and government services, with adoption boosted by “red envelope” giveaways and lottery campaigns.

However, surveys and local reports show that many users still prefer Alipay and WeChat Pay for daily purchases because of their convenience, rewards programs, and deep integration into China’s retail ecosystem.

As a result, e-CNY usage spikes during government campaigns but often falls back once incentives end, highlighting the challenge of turning trial use into lasting behavioral change.

Beijing’s Roadmap for Yuan-Backed Stablecoins

Beijing’s roadmap for yuan-backed stablecoins appears to go beyond simply issuing new tokens.

Reserve-backed stability: State-linked banks are developing reserve models that guarantee full convertibility and transparency, with reserves potentially backed by onshore RMB deposits or short-term Chinese government bonds. This approach allows regulators to monitor flows while preventing arbitrage opportunities.

Targeted pilot corridors: Pilot corridors are being prioritized in Hong Kong and Shanghai’s free trade zones, focusing on trade finance, Belt and Road projects, and commodity imports. These use cases are designed to test large-value settlements without opening China’s entire capital account.

Tight issuance controls: Strict licensing and redemption oversight will ensure that only approved issuers can mint yuan-backed stablecoins, and redemptions can be suspended in extreme cases to protect capital controls.

Transition to Real-World Impact

If successful, this framework could turn Hong Kong into the key liquidity hub for digital RMB assets, enabling exporters and global suppliers to settle invoices in RMB with near-instant finality.

Hong Kong’s Policy Statement 2.0 on the Development of Digital Assets (June 26, 2025) and the HKMA’s work on tokenising trade finance highlight its push to integrate digital assets with the real economy, positioning the city as a testing ground for cross-border RMB settlement.

That would still be far smaller than USD stablecoins, but large enough to start shifting payment flows in Asia-Pacific.

Key Players Driving Yuan-Backed Stablecoin Development

China’s push for yuan-backed stablecoins is not happening in isolation. Major fintech firms, e-commerce giants, and regulators are shaping how this market will grow. Each player brings different strengths, from building the tech rails to setting the rules that make global adoption possible.

Ant Group / Ant International

Ant International (the overseas arm of Ant Group) is preparing to apply for a license in Hong Kong under the new Stablecoins Ordinance (effective from 1 August 2025) to issue fiat-referenced stablecoins.

The company is also exploring stablecoin licenses in Singapore and Luxembourg.

Ant’s interest signals a major shift from China’s earlier strict stance on crypto, indicating that large fintechs are positioning themselves as issuers under the coming regulatory framework.

JD.com

JD.com is actively lobbying the PBOC for approval for offshore yuan-pegged stablecoins, especially for issuance in Hong Kong, as part of its broader push for yuan internationalization.

Its fintech arm “Coinlink” has already made progress in testing stablecoins pegged to the Hong Kong dollar.

JD.com also proposes launching in free-trade zones, to expand usage beyond Hong Kong toward cross-border trade corridors.

PBOC, HKMA, and the Hong Kong/Shanghai Regulatory Strategy

PBOC is central in shaping the roadmap, deciding which entities may be licensed, what reserve-backing and redemption requirements will apply, and how to ensure regulatory guardrails (AML, risk, capital controls) are maintained.

The Hong Kong Monetary Authority (HKMA) has already put into effect the Stablecoins Ordinance as of August 1, 2025, establishing licensing, supervision, and AML/CFT guidelines for fiat-referenced stablecoin issuers.

Meanwhile, Shanghai is being developed as a domestic hub (including an international digital yuan centre) for trials/pilots of yuan-backed stablecoins and related infrastructure under state policy direction.

Comparing e-CNY and Yuan-Backed Stablecoins

Before looking at the road ahead, it helps to see how e-CNY and yuan-backed stablecoins differ in purpose and design. This table summarizes the key contrasts between the two instruments.

“Managed anonymity” (small transactions partly private, large ones traceable)

Permissionless access, higher privacy on public ledgers

Regulatory goal

Enhance domestic oversight and financial stability

Support RMB internationalization while preserving capital controls

Adoption focus

Mainland users and state-driven programs

Exporters, foreign firms, global investors

These distinctions show why China is pursuing both tools simultaneously: e-CNY for domestic control and yuan-backed stablecoins for global reach.

Looking forward, China’s focus will be on proving that both systems can work together without undermining monetary control. Regulators will watch how yuan-backed stablecoins perform in pilot trade settlements and whether they attract global users.

At the same time, e-CNY adoption efforts will likely shift toward encouraging repeat consumer use rather than relying on short-term giveaways. If successful, this combined approach could gradually increase the RMB’s share in international payments and strengthen its position in Asia-Pacific trade flows.

China’s digital currency strategy is no longer centered on a single tool. The e-CNY has proven successful in scaling domestic pilots, reaching 180 million wallets and trillions of yuan in transactions.

However, it struggles to displace entrenched private payment platforms in everyday retail use. Its main strength remains as a state-backed infrastructure for public services, welfare disbursements, and government-driven campaigns.

The push for yuan-backed stablecoins signals a pragmatic policy shift aimed at the global stage. By licensing private issuers, anchoring reserves in onshore assets, and piloting in Hong Kong and Shanghai, Beijing is creating a parallel digital channel that targets cross-border trade and offshore liquidity without loosening capital controls.

Together, the e-CNY and yuan-backed stablecoins form a two-track approach: domestic oversight paired with international flexibility. Their combined success could raise the RMB’s role in global finance, reduce reliance on the U.S. dollar, and reshape how international trade is settled in Asia.

Can foreign companies use yuan-backed stablecoins?

Yes. They are designed to facilitate cross-border payments, making them more accessible to global firms than e-CNY.

Will yuan-backed stablecoins bypass capital controls?

No. They will be regulated with redemption and flow monitoring to preserve China’s capital account policies.

Are these stablecoins pegged 1:1 to the yuan?

Yes. HKMA rules require full backing with cash or equivalents to ensure redemption at par.

Will e-CNY be phased out if stablecoins grow?

No. e-CNY remains the primary domestic rail for retail payments and government services.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Lorena Nessi is an award-winning journalist and media technology expert with 15 years of experience in digital culture and communication. Based in Oxfordshire, UK, she combines academic insight with hands-on media practice.

She holds a PhD in Communication, Sociology, and Digital Cultures, and an MA in Globalization, Identity, and Technology.

Lorena has taught at Fairleigh Dickinson University, Nottingham Trent University, and the University of Oxford. She is a former producer for the BBC in London, with additional experience creating television content in Mexico and Japan.

Her research focuses on digital cultures, social media, technology, capitalism, and the societal impact of blockchain innovation.

She has written extensively on digital media and emerging technologies, with her work featured in both academic and media platforms. Her Web3 expertise explores how blockchain technologies shape culture, economics, and decentralized systems.

Outside of work, Lorena enjoys reading science fiction, playing strategic board games, traveling, and chasing adventures that get her heart racing. A perfect day ends with a relaxing spa and a good family meal.

Easy

Easy